I transformed a high-risk, trust-heavy billing problem into a clearer product system with proactive guardrails

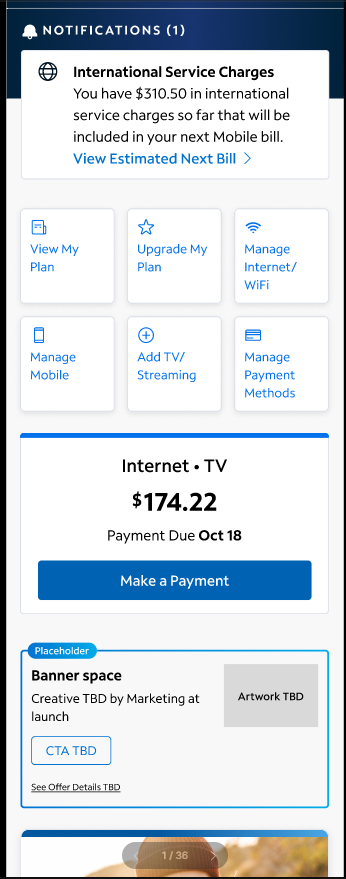

This project started after a customer surfaced a $45,000 international roaming bill, but the real opportunity was much larger than one escalation. Similar complaints pointed to a broader product failure: customers did not understand cost accumulation early enough to make informed decisions.

This was not just a communications problem. It was a complex, trust-heavy financial experience involving billing logic, customer behavior, system rules, payment timing, and service consequences. I helped reframe the issue as a product problem that required earlier intervention, clearer states, and more actionable decision points.

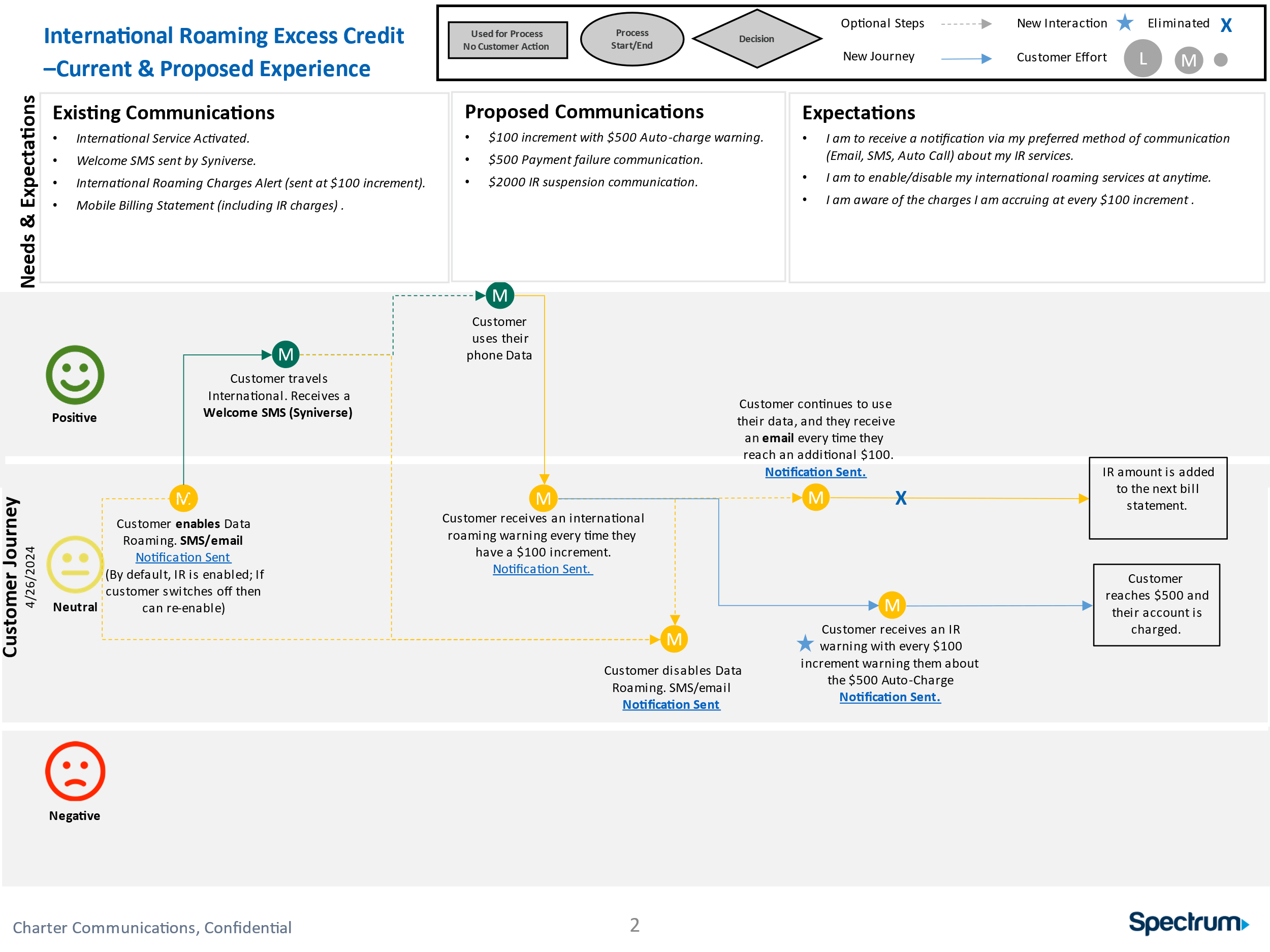

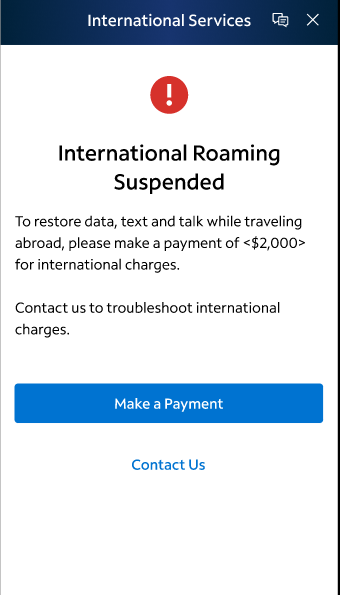

The final model introduced communications at every $100 accrual, auto-charge at $250, and suspension at $1000 if payment failed. My role was to translate that strategy into a coherent customer experience through journey mapping, communication logic, payment and suspension states, and implementation-ready design artifacts.

Overview

International roaming is a strong example of complex product design because the failure was not isolated to one screen or one message. The problem sat across billing logic, payment timing, customer understanding, communications, and service consequences.

My contribution was not just designing UI. I helped shape the product response: defining where intervention should happen, how communication should support the threshold model, and what customer states needed to exist so the experience felt understandable instead of punitive.

- Framed the broader opportunity behind the customer escalation

- Mapped the end-to-end journey and intervention points

- Aligned communication strategy with product and payment thresholds

- Designed key payment, suspension, and recovery states for implementation

- Reduce customer confusion before charges became unmanageable

- Create earlier and more actionable product intervention

- Support revenue collection without relying only on reactive support escalation

- Make consequences and recovery paths clear enough to preserve trust

The customer problem

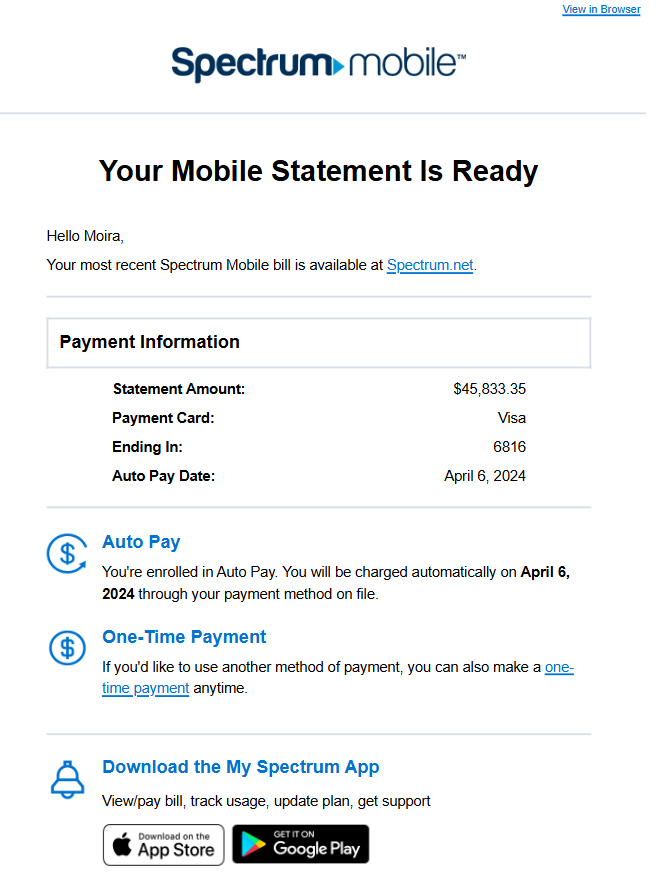

Customers were not intentionally overspending. The system simply failed to make risk visible while charges were accumulating. By the time many customers understood what had happened, the bill was already large enough to trigger panic and distrust.

- “I didn’t know it was adding up this fast.”

- “I would have stopped if I had known sooner.”

- “These charges look fraudulent.”

- Weak in-the-moment visibility into rising charges

- No strong threshold-based intervention path

- No clear recovery flow once payment became urgent

- Fraud complaints and waiver requests

- Higher support cost

- Bad debt when customers refused or could not pay

The intervention model

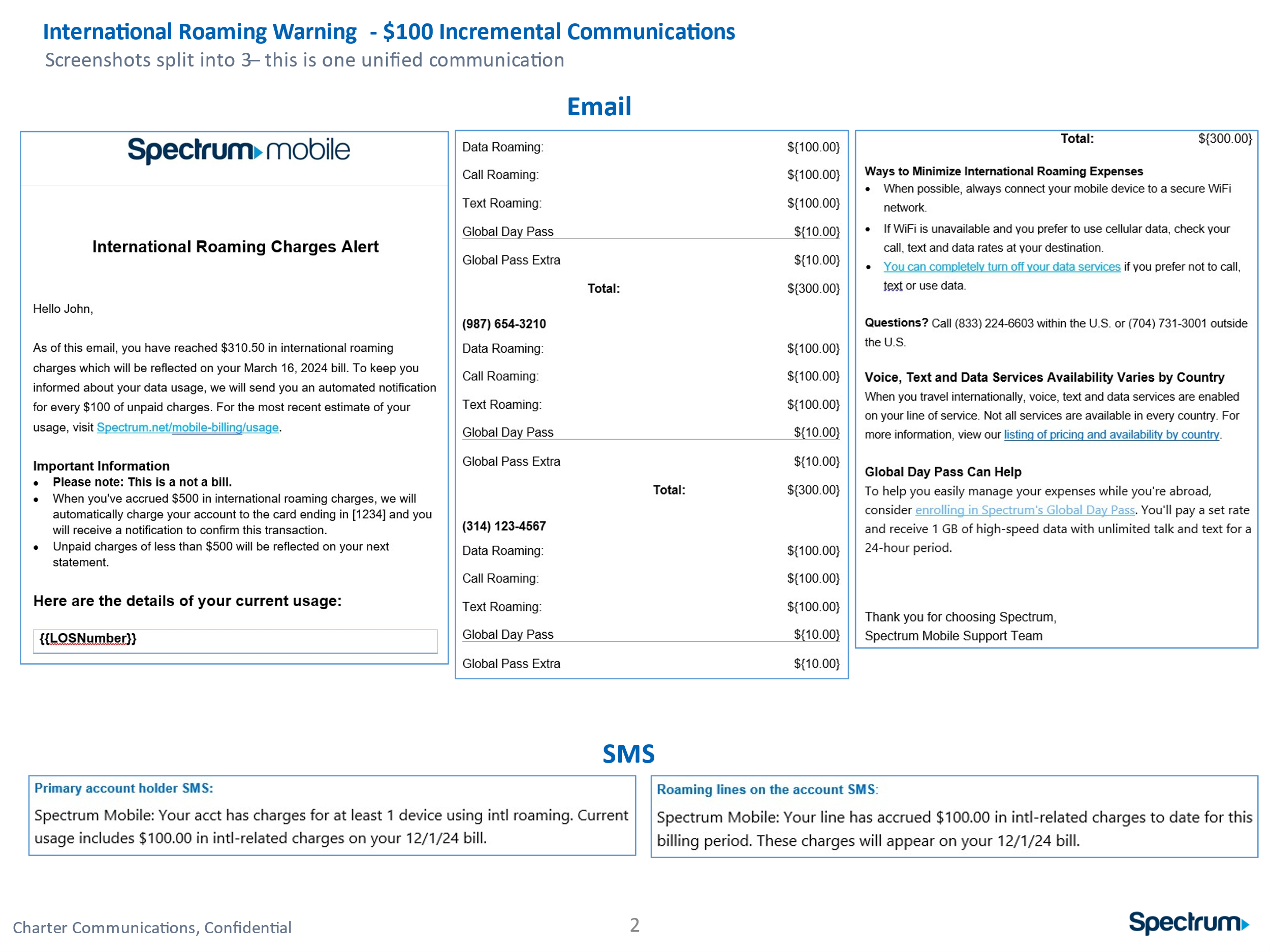

Rather than relying on a single late-stage warning, I helped shape a progressive intervention model. Each threshold was designed to support a different customer and business need: awareness, action, payment, and protection.

Repeated communication at every $100 gave customers multiple chances to understand that charges were rising and that action might be needed.

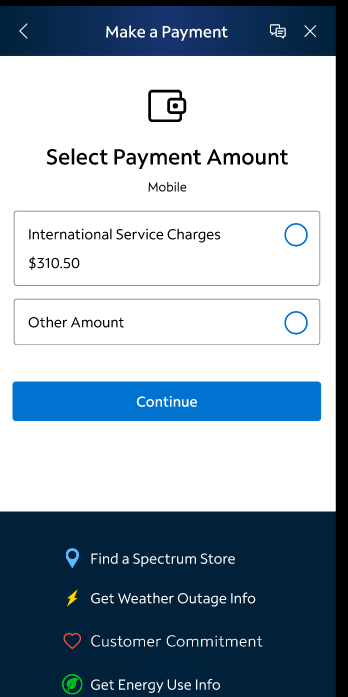

Instead of waiting for the full bill cycle, the system attempted payment much earlier. This reduced lag between charge accumulation and business intervention.

If payment did not succeed and charges kept growing, suspension at $1000 prevented another extreme runaway-cost scenario.

Each communication and screen needed to answer: what happened, what happens next, and what the customer can do right now.

Process

This work required turning a severe customer escalation into a broader product response. I connected complaint patterns, system thresholds, communication timing, payment behavior, and recovery paths into a model that cross-functional teams could align around.

Artifacts

These artifacts prove the work moved beyond abstract policy. They show how I turned system logic into a customer experience that is legible, actionable, and recoverable.

Edge cases I accounted for

High-risk billing experiences do not fail on the happy path. They fail when timing, payment, and customer understanding stop lining up.

- Customers continue using service while charges are growing

- Charge awareness still lags behind behavior, even after initial warnings

- Thresholds may be crossed quickly during heavy roaming usage

- Customers may only react once a payment event becomes real

- $250 auto-charge fails due to decline or insufficient funds

- The customer needs a clear route to update or complete payment

- Suspension at $1000 must feel understandable, not arbitrary

- Reinstatement must be obvious and low-friction once resolved

Impact

The value of this work was not just in sending more communications. It was in shifting the experience from reactive billing to proactive product intervention. Customers gained earlier visibility and clearer action paths, while the business reduced the conditions that led to fraud complaints, waivers, and bad debt.

- Customers were warned repeatedly instead of once

- The business collected earlier with the $250 checkpoint

- The $1000 suspension prevented further catastrophic growth after failed payment

- The UI made the consequence and next action clearer

- I used a real escalation to frame a broader opportunity

- I mapped uncertainty across policy, system behavior, and customer understanding

- I translated ambiguous business logic into a coherent customer experience

- I focused on decision-making, not just deliverables

Reflection

- One severe complaint gets attention, but repeated complaints reveal the system issue

- Customers need intervention points, not just information

- In high-stakes domains, trust depends on making invisible system behavior understandable

- Measure which $100 thresholds most effectively change behavior

- Test comprehension directly: “What happens next?” and “What should I do now?”

- Instrument the recovery funnel from failed payment to successful reinstatement